Contributed by Chaunta Tsegaye, MSA – Insurance Specialist, AAoM

What’s New in Insurance?

On October 19, 2020, Governor Gretchen Whitmer announced that the state is investing more than $1 million and will contact more than one million Michiganders to help provide coverage to those who may have lost health insurance during the COVID-19 pandemic. There are a number ways for people to get no- or low-cost health insurance, and this investment will help raise awareness and increase access to those programs.

ABA News

Telehealth Services might be here to stay. Although many families are beginning to get back into therapy, some families are still opting to have services rendered via telehealth. As the pandemic hit its peak and clinics were forced to close, many families were able to find solace in telecommunication with their ABA providers and receiving instruction to sustain patients until services could again be rendered face-to-face. With this new found modality, insurance companies are considering increasing the time limit to provide these services. Although there are some challenges with connectivity in some areas of Michigan, families could also speak with providers to receive support. If you are in need of a provider, please reach out to our navigator staff (navigator@aaomi.org) for assistance.

Navigating Insurance: Quick Tips and Highlights

We used a common treatment strategy for identifying the most important aspects of information: who, what, when, where, why and how. Here we go:

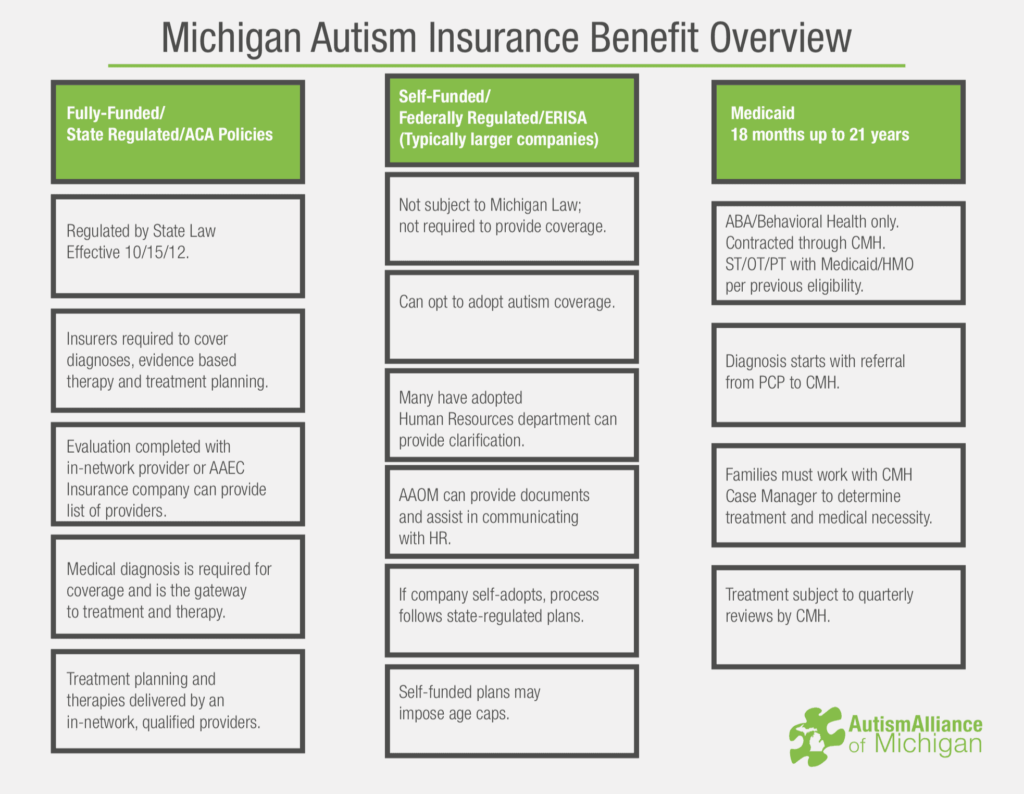

Who are the key players?

- Fully-Funded EmployersEmployers that are fully-funded must offer options that include ASD treatment under Michigan state law.

- Employers Offering Self-Funded Policies

- Employers that offer self-funded policies have the right to choose whether or not to offer the ASD benefit.

- Families who have self-funded policies that do not include ASD benefits can benefit from the purchase of child-only policy options on the Marketplace.

- Employers Offering Self-Funded Policies

If you are renewing your policy on the Marketplace, these are the options available for Michigan residents:

- Blue Care Network of Michigan

- Blue Cross Blue Shield of Michigan

- Mutual Insurance Company

- McLaren Health Plan

- Community Meridian Health Plan of Michigan, Inc.

- Molina Healthcare of Michigan, Inc.

- Oscar Insurance Company

- Physicians Health Plan

- Priority Health

- Total Health Care USA, Inc.

**Quick Notes**

- Your benefits summary should disclose if your plan is fully-funded or self-funded. If not, contact your HR representative to inquire.

- Cheaper premiums do not always equate to savings in the long run!

What should you do?

- If your company is self-funded and ASD coverage is not offered, you should:

- Consult your HR department to inquire about any other insurance options that may be available;

- Search for child-only plans on the Marketplace; or

- Contact MiNavigator for further guidance.

- If you are looking to get a plan through the Marketplace or decide to apply for Medicaid, you should:

- Complete the applications online to receive follow-up information.

- Complete the applications online to receive follow-up information.

- To receive assistance signing up for a Marketplace policy or a quote from an insurance broker:

- Email your name, address and phone number to receive follow-up information.

- Contact MiNavigator for direction to a reputable broker.

When should you apply?

- For child-only policies through the Marketplace, open enrollment begins on November 1, 2020 and ends on December 15, 2020.

- If you are applying for Medicaid, you can apply at any time.

- If your employer offers an ASD benefit, your HR department will inform you of the open enrollment period and deadline for your company.

- Coverage for most plans begins on January 1, 2021; the premium is due at the time you confirm your selection.

- Coverage for most plans begins on January 1, 2021; the premium is due at the time you confirm your selection.

- For plans other than Medicaid, you cannot sign up after open enrollment has ended unless you have a Qualifying Life Event or exception, such as a change in employment, birth of a child, marriage/divorce or death. This is why taking the time to fully evaluate needs during Open Enrollment is critical!

Where do you apply?

- Marketplace and Medicaid

- Applications for the Marketplace and Medicaid should be completed and submitted electronically online.

- Employers

- Your employer will supply this information as well as provide details on how to change/update your policy.

**Quick Note**

- You could potentially have primary, secondary and even tertiary insurance policies.

How do you know if you’ve made the right choice?

There is no foolproof system for making the right decision when it comes to choosing an insurance policy, but here are some factors to consider:

- Are there additional costs beyond my premium?

- Co-pays, co-insurance and deductibles

- Number of hours or sessions incurring co-insurance costs per month

- Access to flexible spending accounts to help offset additional costs

- Are my services covered under the medical or mental health benefit?

- Applied Behavior Analysis (ABA)

- Speech (SLP), Physical Therapy (PT) and Occupational Therapy (OT)

- Are my preferred providers In-Network with the selected plan?

- Are there visit or hour limits applied for services rendered in the plan?

Why is this important?

Most of us already know, but the hustle and bustle of life can interfere with time-consuming evaluation and decision-making surrounding open enrollment. It’s easy to overlook considerations and limitations of policies. The most important “why”, however, is: “Why doesn’t the law passed in 2012 apply to me?” The Michigan Autism Insurance Reform passed in 2012 mandated ASD treatment for children. Michigan is headquarters, however, to many self-funded employers across the state that are not bound by state law, but rather regulated by federal policies and decisions at the discretion of the employer.

The Paul Wellstone and Pete Domenici Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA) is a federal law that generally prevents group health plans and health insurance issuers that provide mental health or substance use disorder (MH/SUD) benefits from imposing less favorable benefit limitations on those benefits than on medical/surgical benefits.

CMS Parity does not require an employer or insurer to provide coverage. Should you have any questions or need additional assistance, please contact the MiNavigator program.